Global Head of Consultancy Rob Morris was joined by Chris Seymour, Head of Market Analysis, alongside Senior Consultant Richard Evans and Senior Aviation Analyst Connor Diver for Ascend by Cirium’s last webinar of the year.

The speakers shared their insights on how recovery has progressed in the passenger and cargo markets, and the outlook for 2023 and beyond. Read on for our key takeaways from the live broadcast which drew on the latest Cirium data.

2022 has been a year of sustained demand recovery, with slow and steady growth in Asia

Connor Diver began the presentation by examining capacity trends since the start of the pandemic, drawing on Cirium Schedules data. The Intra-Europe and US-domestic markets were strong in 2022, recovering to 2019-levels at points despite several factors constraining capacity, such as airport staffing shortages.

Elsewhere, after two years of turmoil the Intra-Asia market improved consistently, a trend set to continue into 2023. “Despite starting the year at 60% down over 2019 levels, through slow and steady growth through the year, the Intra-Asia market is now 40% down” noted Connor. While heavily influenced by the situation in China, where Covid-19 restrictions have produced a volatile domestic market, the wider region has seen a sustained recovery that is set to continue into 2023.

In long-haul markets, the Trans-Atlantic recovery that began in Q4 2021 continued, with traffic now close to year-over-2019 and projecting positive heading into the new year. While the Trans-Pacific and Europe-Asia markets lag, they have also made slow and steady progress as demand in Asia continues to rebuild. Connor concluded that these two markets are the ones to watch in 2023.

Market values and lease rates for twin-aisles are past the worst

Connor also assessed how market values have developed through the year. The recovery of single-aisle values that began in 2021 continued through 2022 and are now firmly in recovery. 2022 marked a turning point for twin-aisle values, also now on a positive trend as long-haul demand returns. Connor pointed to several newer twin-aisle types now firmly in recovery, with older types past an inflection point and rising again. These trends have been mirrored in lease rates, with some single-aisle types already above 2019, and twin-aisle rates set to continue recovering back towards pre-pandemic levels.

Turning to the leasing market, Connor noted that leases for widebodies have hit record levels, with more leases in 2022 so far than in any year of the previous cycle. “In addition to the underlying market recovery, lease rates are still fairly attractive verses pre-pandemic levels, especially on widebodies, and ultimately there is cheap capacity out there” he explained. “You also have to consider what other options airlines have; OEM production rates have remained very low, anything that’s being built now is facing supply chain issues, and there’s a backlog to clear.”

Meanwhile, Fleets Analyzer data shows the twin-aisle lessor idle fleet has remained stable despite these record leases, in contrast to the declining availability of single-aisles. Connor explained this reflects the older profile of parked widebodies, and an anaemic trading market dampened by the higher cost of capital and sellers waiting for prices to recover towards book value. This has contributed to a slower than expected part-out market, another area to watch in 2023 as lessors struggle to trade aircraft out from the back end of their portfolios.

As freighter orders pile up, growth in the cargo market is slowing

Chris Seymour examined the cargo market in depth, starting with traffic and capacity trends. Having suffered less than the passenger sector in 2020, freighter traffic rebounded strongly in 2021, growing by 6%. However, growth has slowed as 2022 has progressed, with the positive outlook at the start of the year eroding as the Ukraine-Russia conflict, continuing lockdowns in China, and looming recession all impact trade flows.

Global cargo capacity remains 8% below pre-Covid levels, with long-haul belly capacity still to fully return, but the number of dedicated freighters has grown substantially; the narrowbody fleet is 22% larger than at the outset of the pandemic, driven by ecommerce growth and new market entrants. New-build freighter orders have been boosted in the last two years, and conversions have boomed; Ascend has tracked over 700 orders, with 2022 on course to be a record year of deliveries.

With dedicated capacity set to grow as demand slows, will a surplus of supply form as belly capacity returns? Chris’ verdict: “Yes, potentially we may see that – maybe all the conversion orders being placed now is the peak and we’ll come back to long-term trends in the mid- to late-2020s”, warning that there may be too many conversion lines for the market to fill by the middle of the decade. However, high levels of ecommerce activity, supply chain issues and labour woes are all set to continue, suggesting the pre-pandemic status quo will not return.

2023 and 2024 will be recovery years

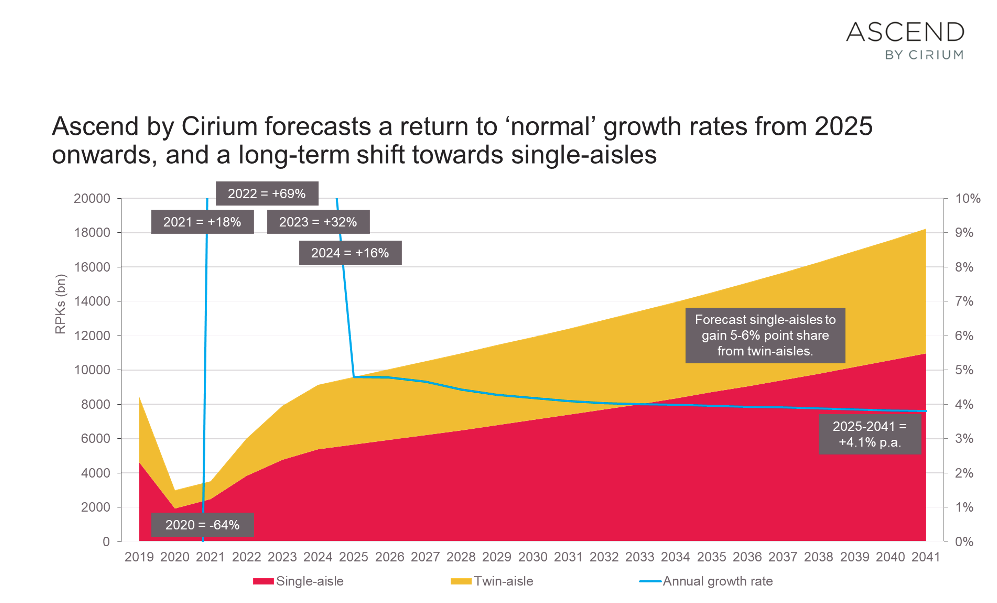

Richard Evans shared his analysis of the passenger market, starting with Ascend’s updated recovery scenario. In traffic (RPK) terms, Ascend now projects global volume in 2022 to be 30% below 2019, before recovering to pre-Covid levels in October 2023. The passenger fleet is on course to match pre-pandemic numbers in May next year, growing ahead of traffic with single-aisles comprising an increased share of the overall fleet.

Although RPKs and fleet numbers will match pre-pandemic levels in 2023, growth rates will take longer to return to ‘normal’. Ascend projects a compound traffic growth rate of 3.6% between 2019 and 2041, down from 4.5% for its 2018-2038 forecast representing three to four years of lost traffic by the 2040s. “We’ve gone from a market where we said passenger traffic growth is 5% per annum, then four-point-something, and now three-point-something” observed Richard.

Both short- and long-term factors underlie the reducing growth rate forecasts. Airlines are still in a recovery phase and have capacity decisions to make with higher debts. In the long-term, GDP growth and falling costs are the two main drivers of passenger growth; forecasts are being cut and costs are rising. Richard points to decarbonising aviation as the major long-term challenge. “The big debate is whether the costs will be offset by fuel burn reductions that technology brings; in our view, probably not” Richard explained, concluding that how the industry addresses climate change will be key to long-term growth.