READ ALL OF THE LATEST UPDATES FROM ASCEND CONSULTANCY EXPERTS WHO DELIVER POWERFUL ANALYSIS, COMMENTARIES AND PROJECTIONS TO AIRLINES, AIRCRAFT BUILD AND MAINTENANCE COMPANIES, FINANCIAL INSTITUTIONS, INSURERS AND NON-BANKING FINANCIERS. MEET THE CIRIUM ASCEND CONSULTANCY TEAM.

How did we get here?

By Michael Graham, Valuations manager at Ascend Consultancy

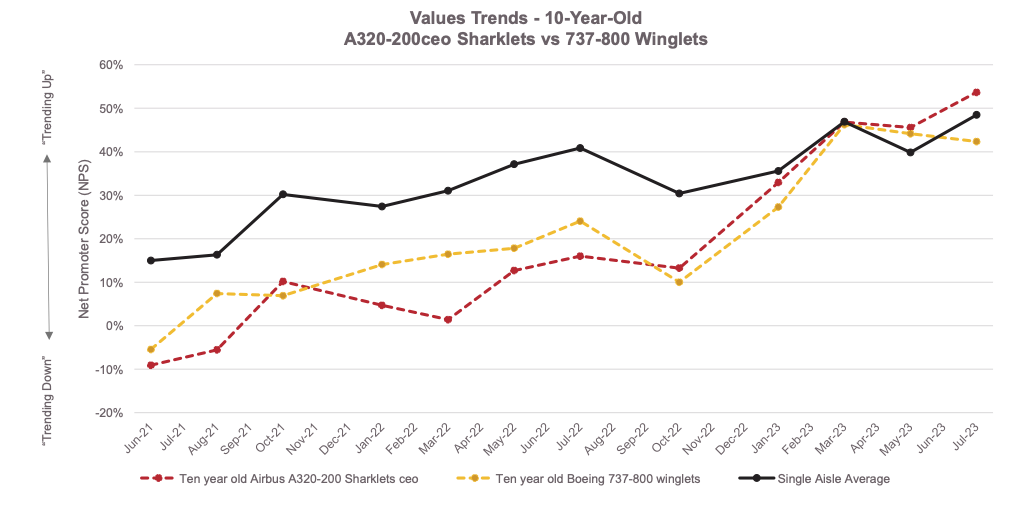

Within CAMSI, we utilise a Net Promotor Score (NPS) Index methodology – calculated as the number of respondents replying ’too high’ or ‘trending up’ minus those replying ‘too low’ or ‘trending down’, divided by the total sample response to that question. Scores in the 40% to -40% range broadly indicate stability, those below -40% can be considered to indicate a negative sentiment and those above 40% indicate a positive sentiment.

“And you may find yourself in another part of the world, and you may find yourself behind the wheel of a large automobile…. and you may ask yourself, “Well, how did I get here?” The question posed at the start of Talking Heads’ 1981 hit, Once in a Lifetime is pertinent when looking at where we are in terms of the recovery in commercial aircraft Market Values and Lease Rates, especially given the challenges emerging in terms of the supply of aircraft which have rapidly come to a head over the past 12 months.

When CAMSI started in April 2021, trends for both aircraft Values and Lease Rates were firmly in negative territory. Storage rates, particularly for older aircraft, were through the roof and stringent travel restrictions and vaccination coverage limited in many markets meant that demand for many aircraft types had almost collapsed. With the benefit of hindsight, it is easy to see that eventually demand, along with aircraft Values and Lease Rates would recover. However, the nature of the recovery in NPS for Values and Lease Rates has thrown up some noteworthy trends in recent months.

In May, June and July’s CAMSI surveys on Market Values and Lease Rates we saw NPS for 2013-build Airbus A320-200 Sharklets and Boeing 737-800 Winglets climb above the overall single-aisle average for the first time.

In other words, according to our respondents, Values and Lease Rates for mid-vintage aircraft are trending upward more strongly than for their new-build successors.

While this may turn out to be a temporary phenomenon, it marks a dramatic reversal of fortune and speaks to a number of realities now facing the market for passenger aircraft.

Chief among these realities is the aforementioned lack of supply of new aircraft, manifesting in delivery delays to airlines and lessors. Both airframe and engine OEMs saw their supply chains decimated during the pandemic and are still scrambling to recover. According to our 2022 Cirium Fleet Forecast, Airbus remains at least two to three years away from its mid-term goal of producing 75 A320 family aircraft per month and in Renton, WA the picture is not much rosier. Boeing’s monthly production rate of the previously beleaguered 737 Max, while having climbed to 38 in recent months, is still far below its pre-grounding and pre-pandemic peak of 52 aircraft per month.

The consequent aircraft delivery delays are predictably creating significant operational headaches for airlines.

In April, Airbus issued a statement confirming that delivery delays of a minimum three months on its A320neo family aircraft may run into 2024. While this apparent mea culpa may have offered a useful degree of visibility for airlines, the fact remains that not having their new aircraft in time for the traditional summer peak season, is about as useful as a snooze button on a smoke alarm. Furthermore, a delay of three months has now come to be seen as a good outcome; delays of six months or more are becoming much more common. That said, it is worth remembering that through these challenges, many airlines have also been able to capitalise on their lack of capacity through higher fares – as ever, it is the passenger who ultimately pays.

Not to be left out, engine OEMs have seen their fair share of challenges, most notably in terms of the on-wing reliability for their latest generation powerplants and particularly the Pratt & Whitney PW1100G and CFM Leap. In a recent announcement, Pratt & Whitney stated that it had determined that a rare condition in powder metal used to manufacture certain engine parts will require “accelerated fleet inspection” which is likely to lead to further challenges to aircraft supply, as aircraft may have to be temporarily removed from service for inspection. This is in the context of MRO facilities which are already stretched in terms of availability.

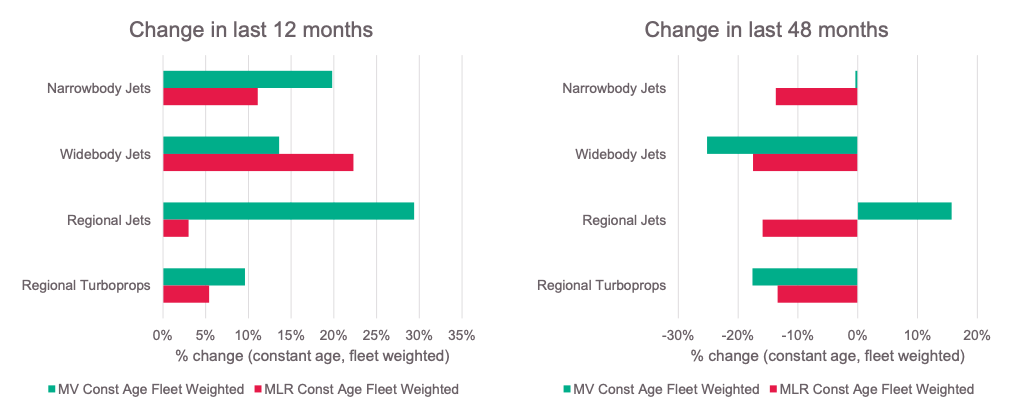

All of which leads to the question of what effect this is having on aircraft Market Values and Lease rates. As we have written before on Thought Cloud, the constrained supply of new-build aircraft in the face of burgeoning demand can eventually drive Values and Lease Rates for older aircraft upwards, as airlines seek out alternative means of rebuilding capacity. In recent months the Cirium Ascend Consultancy Values Review Board has increased its Current Market Value opinions for the A320ceo Family by up to 29%, while 737NG Values have risen by up to 28%. Even older widebodies, which have previously been seen as laggards, have had their recoveries move up a gear in recent months. In June our Airbus A330 Market Lease Rate opinions saw increases of up to 30%, depending on vintage, albeit from a low starting point. This followed Lease Rate increases of up to 23% and 17% for A320ceo family and 737NG aircraft respectively in late Q2, based on extensive data capture.

The final piece in the puzzle is aircraft lessors. One might imagine that in this new world of rising Lease Rates, lessors are in a position of strength, as I wrote back in April. However, while a shift in the balance of supply and demand may have allowed lessors to charge higher rents as evidenced above, for many their cost of capital has also increased, placing pressure on margins.

Intense competition between lessors, particularly within the all-important single-aisle market, has also served to moderate Lease Rate rises, in turn keeping lease rate factors subdued.

Indeed, on a fleet-weighted average basis, while narrowbody aircraft have now almost recovered to pre-pandemic levels in terms of Market Values, Lease Rates remain some 14% lower. This is almost unprecedented, as nearly every previous recovery from a downturn in the last 40 years has been Lease Rate led.

So what are we to make of the latest results from CAMSI and the what they may reveal about the ongoing post-Covid recovery? Firstly, it is clear that a constrained supply of new aircraft in the face of burgeoning demand is the key factor in driving up both Market Values and Lease Rates, often right across the vintage spectrum. Secondly, lessors, while now more able to drive up rents are not having it all their own way as intense competition moderates their pricing power. However, while airlines, OEMs and lessors are facing a smorgasbord of challenges, after the financial and human trauma of the pandemic one cannot help thinking that these are now much nicer problems to have.

As always in the cut-throat world of commercial aviation, the question should not be “How did I get here?”, but rather, “Where are we heading next?”

We are always looking for further respondents to reflect all aspects of the market, who can then benefit from receiving the full set of results (above is only a top line summary). The CAMSI survey takes only 3min to complete yet provides respondents with the most comprehensive picture of the aircraft value market trends available. If you would like to participate, please contact youcef.berourminarro@cirium.com. Participants will receive a complete and detailed analysis of the survey results, with 10 or more graphics included.